The infrastructure gap has been growing across Southeast Asia, with India, Indonesia, and the Philippines requiring high levels of private and institutional financing to achieve national objectives and meet international climate commitments. Framed by the G20 Principles for Quality Infrastructure Investment, this chapter identifies three priority areas that shape the investment climate: land acquisition and ownership, innovative financing mechanisms, and the integration of environmental, social and governance (ESG) considerations. Barriers to investment include fragmented regulatory frameworks, lengthy approval and permitting processes, inconsistent coordination between levels of government, and limited standardisation of reporting.

Addressing Legal and Regulatory Barriers to Quality Infrastructure Investment in India, Indonesia and the Philippines

Abstract

This report is part of the OECD's multi-year project on legal and regulatory barriers to quality infrastructure investment in Asia, focusing on India, Indonesia, and the Philippines. Previous OECD work found that investors repeatedly identified legal and regulatory barriers as a primary impediment to infrastructure investment (Financial Stability Board, 2017[1]). The objective of this research is to bring better understanding to the policy actions that could be taken to attract quality private financing to infrastructure projects, which are by nature multi-year investments and have complex structures.

The three countries are expected to require the highest level of climate financing in Southeast Asia (ADB, 2024[2]). The International Finance Corporation (IFC) estimates that India will need around USD 10 trillion to reach its net-zero targets in 2070 (International Finance Corporation, 2023[3]). Indonesia’s Bappenas’ latest estimates place climate finance needs at USD 40 billion until 2025, and at USD 270-350 billion between 2026 and 2030 (Bappenas, 2021[4]). The Philippines has no net-zero targets, but its National Development Company’s (government investment arm) submitted plan as part of its Nationally Determined Contribution (NDC) under the Paris agreement in 2020 expects to avoid seventy-five percent (75%) of GHG emissions between 2020 and 2030. The availability and ability of private financing to support this will be critical for these investment levels to be met.

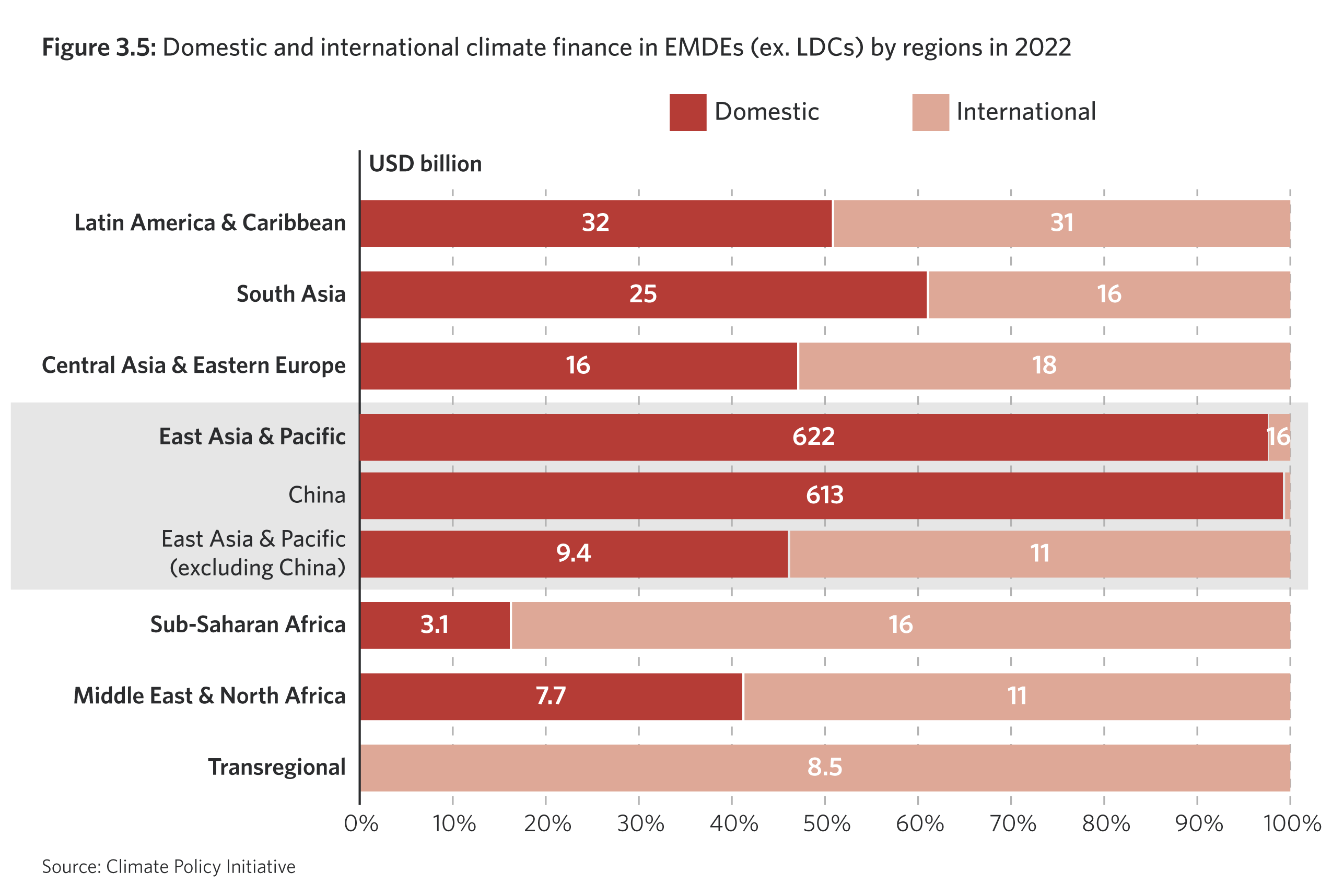

South Asia, in particular, is a popular climate finance destination for global investors, (Climate Policy Initiative, 2023[5]) and external factors function to support financial institutions providing more sustainability-oriented products. (Slaughter and May, 2024[6]) While the accumulated volume of sustainable finance products are still high, net inflows/issuance into sustainable funds and sustainability bonds peaked in 2021. (UNCTAD, 2024[7]) Regulatory measures such as the EU’s Corporate Sustainability Reporting Directive (CSRD) and Corporate Sustainability Due Diligence Directive (CS3D) are being reviewed, but they will probably continue for companies, and will likely drive sustainable finance forward.

This report has been developed through a combination of desk top research and interviews with relevant government officials, national institutions and private investors. The project has taken an iterative approach to identify key areas of concern for private investors and develop inputs to inform the three countries. This report synthesises findings from interviews and desk research conducted in 2023 and 2024. While findings remain relevant, the primary insights reflect conditions during that period. The three areas were identified to be explored further taking into consideration the G20 Principles on Quality Infrastructure Investment (G20, 2022[8]).

The first is land acquisition, ownership, and right of way challenges. There is a need for stronger alignment between national and local regulation, and for openness to foreign investment. In all three countries, approval, bidding, and award processes are lengthy and complex, and ownership structures are not completely liberalised. This lack of clarity on rights to access extends negotiations periods, and can require further impact assessments, concessions for easements or compensation. This issue can be addressed through fostering alignment between the enforcement of open regulations at the local level and federal state regulator, to increase openness towards foreign investors looking to participate in infrastructure projects. In facts, better regulatory coordination between jurisdictions, as well as initiatives like harmonised national project lists can contribute to reducing regulatory discrepancies and duplication and to providing more clarity and attractiveness of project pipelines.

Quality infrastructure investment is essential for driving economic growth, enhancing productivity, and improving human well-being. Achieving these benefits requires governments and stakeholders to work together to establish robust policies and governance frameworks that ensure effective planning, financing, and oversight of projects. Developed under Japan's 2019 G20 Presidency, the G20 Principles for Quality Infrastructure Investment offer a voluntary framework to guide countries in making infrastructure investments that maximise economic, social, environmental, and developmental benefits.

These principles emphasise the importance of sustainable and resilient infrastructure, economic efficiency, inclusive development, environmental sustainability, transparency and accountability, and innovation. Quality infrastructure is therefore a foundation for inter alia:

Providing access to clean drinking water and sanitation which are fundamental for health and economic productivity.

Mitigating flood risks and improving access to water through improved storage for multiple water uses, such as irrigation, manufacturing and hydropower.

Improving access to clean and low-emission electricity.

Providing reliable and accessible low-emissions transport - a key contributor to improving livelihoods and economic productivity.

Expanding Internet access and telecommunication services that give rise to increasing connectivity and generate economic opportunities.

Delivering social services such as health, education and affordable housing, which are essential for human development and the reduction of inequalities.

Building sustainable, inclusive and livable cities.

Improving cross-border connectivity which is essential for supporting trade, integration into regional and global value chains, and inclusive growth.

Ensuring sustainable use of natural resources, and low-carbon and environmentally responsible societies.

To achieve such positive outcomes, infrastructure investment should be guided by a sense of shared, long-term responsibility for the planet consistent with the 2030 Agenda for Sustainable Development, national and local development strategies, and relevant international commitments, and in the spirit of extensive consultation, joint efforts and shared benefits. Domestic resource mobilisation is critical to addressing the infrastructure financing gap. Assistance for capacity building, including for project preparation, should be provided to developing countries with the participation of international and regional organisations and development institutions and agencies.

Source: (OECD, 2021[9])

This corresponds to Quality Infrastructure Investment (QII) Principle 2 on raising economic efficiency in view of life-cycle cost by having some certainty over the process of land acquisition, Principle 3 which expects environmental impact of infrastructure investment to be made transparent to all stakeholders, as well as Principle 6 which calls for openness and transparency of procurement process. (G20, 2022[10])

The second area is the availability of more innovative and alternative investment vehicles or financing mechanisms. This can encourage the development of an ever more enabling environment for foreign investment. Blended finance instruments are crucial in addressing challenges in the deployment of capital, particularly for unbankable or marginally bankable projects. Larger ticket projects can be more attractive to private and institutional investors and are useful to enhance blended finance platforms. Investment platforms – rather than straight assets – might provide better sizable and scalable opportunities for private investors. Through partnerships with local private investors, banks, or Multilateral Development Banks (MDBs), investors may have more resources to negotiate better incentives and guarantees while finding a sounder balance between their cost and their effectiveness.

This corresponds to Principle 2 of QII in terms of using innovative technologies to be leveraged through the life cycle of infrastructure projects to raise economic efficiency (G20, 2022[10])

The third area is integrating Environmental, Social, and Governance (ESG) considerations in infrastructure project preparation and structuring. This will contribute to better aligning projects with investors' long-term investment strategies and compliance requirements. In most countries in the South and Southeast Asian region, emerging ESG considerations still require regulatory reform to match private investors' compliance requirements and facilitate their access to the market. Fostering public-private dialogues will be instrumental in integrating ESG considerations into the decision-making process and collaborating in identifying ESG compliant financial instruments for infrastructure, such as green bonds. Moreover, the integration of ESG considerations in infrastructure projects will facilitate compliance with ESG reporting requirements, including measurement.

This corresponds to Principles 3 and 5 of the QII, on integrating environmental and social considerations in infrastructure investments (G20, 2022[10]).

Despite unique challenges and opportunities, the three countries share common goals: streamlining processes, integrating public-private partnerships (PPPs), and embracing sustainability to attract private foreign investments. Taken together, these measures can improve the long-term bankability and sustainability of infrastructure projects in each country.

The three countries have been particularly effective in working with investors to form partnerships with local entities and MDBs to diversify into blended finance instruments for infrastructure. Some projects have been too small for debt instruments, such as syndicated loans through special purpose vehicles (SPVs), and such approaches can accommodate financing for diverse projects.

Each country has introduced several initiatives to diversify their financing options to support private investment. Development of a pipeline of projects and PPP procedures for various large projects have contributed to ensure greater clarity of investment opportunities that may be available. Establishment of banks and funds in India and Indonesia that are mandated to contribute to infrastructure project development injects financial market expertise into financing, which can lead to better project outcomes.

Generally, the region faces sovereign credit risk ceilings which can hamper access to international capital markets for foreign currency funding. Institutional investors like pension funds may have limitation due to home country financial regulation to invest in infrastructure assets abroad or through country credit rating requirements. The level of capital market development will also impact the availability of financial instruments available, as the depth and liquidity of local markets will determine the types of instruments that can be reasonably made available and traded.

Regulatory reforms to strengthen institutions and frameworks, as well as streamlining and disclosing administrative processes would greatly benefit all three countries. While India has made much effort to centralise processes, ensuring that institutions responsible are applying regulations and processes consistently across the projects is essential for all three countries. Furthermore, countries not only want to facilitate more investment but also attract investment from funds that have a positive impact in their countries and on their infrastructure.

Local governments often struggle to meet the strict project preparation and implementation standards required by relevant MDBs due to capacity constraints, as well as patchy coordination with the national government, with regulations and guidance not always being applied consistently. Better coordination with local governments on permits as well as land acquisition should be considered. Land acquisition involves issues such as pricing compensation and supporting indigenous people’s rights. The local government would need to play a key role to ensure that such issues can be addressed in an appropriate manner if project development is to take place. Early discussions with local authorities and highlighting of potential local considerations could avoid delays in addressing such issues at a later stage.

Developing ESG standards to investment that meets international standards and can be externally verified is necessary to attract foreign investors. Indonesia has in particular been actively developing domestic standards. India has also taken a number of steps to advance ESG standards. Ensuring that these standards adhere to international acceptable levels will be important.

State-owned enterprises (SOEs) are key infrastructure players in many countries, as is the case in these countries. Their corporate governance will inform their decision-making process, as well as how the market perceives their business practices. Reviewing whether their decision-making can contribute to the long-term infrastructure planning, and how they can better contribute to this will be essential.

The report includes country sections and a list of good practices and policy recommendations for each country, taking into consideration the specific circumstances of them. The context by which the country operates its infrastructure assets and services, as well as the financing circumstances is elaborated in each section.

With these high-level observations in mind, the three countries may wish to consider the following recommendations to improve their infrastructure financing regime:

Create clearer and streamlined processes on land acquisition, ownership, and right of way to establish the requirements and approvals needed to develop infrastructure projects and ensure transparency of the process, in particular in coordination with local authorities. Challenges of land acquisition and ownership are unanimously highlighted by investors as one of the main barriers. In all three countries, approval, bidding, and award processes are lengthy and complex, requiring streamlining to provide investors with a more transparent and attractive framework for investment, particularly concerning Indigenous Peoples' rights. Indonesia's Land Bank and India's digitisation of land titles are attempts to address this issue, while the Philippines’ conglomerates dominate construction and infrastructure sectors which can slow progress.

Address regulatory complexity, discrepancies, and inconsistencies between the national and local governments. All three countries face challenges with fragmented regulatory environments and would benefit from better harmonisation of national and local regulations. Simplifying and standardising approval, permitting, and compliance processes would reduce bureaucratic delays and attract private foreign investments.

Standardise reporting requirements and disclosure on financial as well as non-financial information to support a better understanding of the infrastructure financing landscape of the country, and support considerations by foreign investors.

Develop and apply ESG standards more consistently, ensuring the ESG standards adhere to internationally recognised levels. In addition, such ESG standards should be verified by an external party, which has the expertise to carry out such verifications and be aligned as sustainable finance opportunity. These measures could reinforce the improvements to data and transparency, regulatory streamlining, and governance stability achieved above, to further advance the sustainability of infrastructure in the region.

Strengthen corporate governance of SOEs in line with listed companies and make their business model commercially oriented if they want to attract foreign investment. Ownership structure as well as potential listing on the stock exchange should take place in the context of better management, as well as financial sustainability and business opportunity of the SOE to ensure that it can contribute to the business of the SOE/infrastructure asset in the long-term and contribute to operation and maintenance of the relevant infrastructure services.

References

[2] ADB (2024), ASIA–PACIFIC CLIMATE REPORT 2024: Catalyzing Finance and Policy Solutions, https://www.adb.org/sites/default/files/publication/1008086/asia-pacific-climate-report-2024.pdf.

[4] Bappenas (2021), A Green Economomy for a Net-Zero Future: How Indonesia can build back better after Covid-19 with the Low Carbon Development Initiative (LCDI), https://lcdi-indonesia.id/wp-content/uploads/2021/10/GE-Report-English-8-Oct-lowres.pdf (accessed on 3 September 2024).

[5] Climate Policy Initiative (2023), Domestic and International climate finance in EMDEs (ex. LDCs) by regions in 2022, https://www.climatepolicyinitiative.org/wp-content/uploads/2023/10/Figure-3.5.png.

{kind=link}

[1] Financial Stability Board (2017), FSB discusses 2018 workplan and next steps on evaluations of effects of reforms, https://www.fsb.org/2017/10/fsb-discusses-2018-workplan-and-next-steps-on-evaluations-of-effects-ofreforms/.

[8] G20 (2022), Compendium of Quality Infrastructure Investment Indicators, G20 Infrastructure Working Group, https://cdn.gihub.org/umbraco/media/4761/compendium-of-qii-indicators.pdf (accessed on 19 December 2023).

[10] G20 (2022), Compendium of Quality Infrastructure Investment Indicators, https://cdn.gihub.org/umbraco/media/4761/compendium-of-qii-indicators.pdf.

[3] International Finance Corporation (2023), Blended Finance for Climate Investments in India, https://www.ifc.org/content/dam/ifc/doc/2023/Report-Blended-Finance-for-Climate-Investments-in-India.pdf (accessed on 3 September 2024).

[9] OECD (2021), Using blended finance to unlock commercial investments, https://www.oecd-ilibrary.org/sites/5efc8950-en/index.html?_csp_=6f524d6f7dc250ba913c88ad8727c82b&itemContentType=book&itemIGO=oecd&itemId=%2Fcontent%2Fpublication%2F5efc8950-en (accessed on 3 September 2024).

[6] Slaughter and May (2024), Sustainable Finance Re-examined, https://www.slaughterandmay.com/insights/new-insights/sustainable-finance-re-examined/.

[7] UNCTAD (2024), World Investment Report - Investment facilitation and digital government.