Women-led businesses are substantially less likely to sell their products and services internationally than those led by men. Consequently, they are less able to seize the opportunities for increased competitiveness, greater economies of scale and other benefits from trade. There are several reasons for this: women-led firms tend to be smaller, and larger firms tend to trade more. Women also tend to lead businesses in sectors where trade is less prevalent like services. Women are also more likely than men to lead businesses that are in the informal economy. Firms that trade are substantially less likely to operate within the informal economy in part because exporting requires strict adherence to official requirements. Women business leaders indicate that they are held back from engaging in trade due to factors such as a lack of understanding of foreign markets which may reflect a broader informational gender gap that could be closed with targeted policy solutions.

Trade and Gender Review of Latin America

Abstract

Firms involved in international trade tend to be more productive than those that do not trade and engaging in international trade improves firm performance: exporting leads to market expansion and sales growth, can bring productivity gains from greater competition, and may induce innovation and generate knowledge spillovers (Bernard, 2007[1]). However, women-led businesses are substantially less likely to sell their products and services internationally than those led by men. Consequently, they are less able to seize the opportunities for increasing competitiveness, greater economies of scale and other benefits from trade.

Ensuring that businesses led by women entrepreneurs are able to take advantage of opportunities provided on international markets will support greater gender equality and help to close gender gaps, in addition to contributing to higher and more inclusive economic growth.

This chapter examines the presence and challenges of women business leaders in trade and the specific obstacles they face. The analysis covers Latin American firms from Argentina, Brazil, Chile, Colombia, Costa Rica, Mexico and Peru, and uses data from the OECD-World Bank-Meta Future of Business Survey (Box 3.1) as well as a series of round tables that were held with women entrepreneurs and business leaders in Brazil, Colombia, Costa Rica, Mexico and Peru. By examining the factors contributing to gender disparities in exports and uncovering the specific barriers encountered by women leaders, this analysis aims to provide insights for addressing these challenges effectively.

This chapter makes use of data from the OECD-World Bank-Meta Future of Business Survey of firms with an online presence on Facebook. The bi-annual Future of Business survey includes questions about perceptions of current and future economic activity, challenges, strategy, and business characteristics, including the gender of the owner/manager. The survey aims to give a snapshot of small and medium-sized businesses with an online presence. Over 700 000 Facebook page owners have taken the survey, out of a population of 90 million businesses that have created a Facebook business page. The survey can be accessed at: https://datacatalog.worldbank.org/dataset/future-business-surveyaggregated-data.

A questionnaire on firm characteristics and economic activity was distributed to a random sample of businesses in March and October 2022. This resulted in information on almost 4 000 businesses in LAC countries, including whether or not they engage in trade, the gender make-up of their leadership, and other business characteristics such as size and sector of activity.

Firms are defined in this analysis as women-led if they report that the majority of their leadership is women, with the reverse for men, while equal-led businesses are those with a 50-50 division at the time of the survey. Among the surveyed firms, 24% indicated they were women-led, 38% were equal-led and 38% were men-led.

In the analysis of the survey data, firms are weighted in order to ensure the random sample resembles the population of Facebook page administrators. (More information on the weights and the survey are in (Schneider, 2020[2]). Since this group is not identical to the wider business population, the survey should be regarded as representative of firms with an online Facebook presence rather than businesses generally.

Evidence from the survey of firms with a presence on Facebook shows that men in Latin America are much more likely to run businesses than women. Less than one-quarter of businesses are run primarily by women whereas over one-third are run by predominantly male leadership teams. The under-representation of women leaders is particularly pronounced in Argentina and Mexico, where women lead only 18% and 21% of enterprises, respectively (Figure 3.1).

Note: This graph shows the share of businesses with a presence on Facebook that indicated that their leadership consists of mostly women, mostly men, or about equal numbers of men and women.

Women-led businesses in Latin America with a Facebook presence are less likely to participate in international trade compared to those led by men. This export gender gap is roughly 4 percentage points: 10% women-led firms are engaged in international trade, compared to 14% for male-led firms. The gender-export gap is wider in Mexico and Costa Rica, and narrower in Colombia, Brazil and Peru (Figure 3.2). Both women-led and men-led firms in Latin America export less compared to their counterparts in the OECD. However, the gender export gap in the Latin American countries is smaller than in the OECD, which indicates that lower levels of export do not only plague women-led firms.

The export gender gap can be attributed to several factors linked to the characteristics of women-led and men-led businesses such as their size and the sectors in which they operate. Women led firms tend to be smaller and younger and operate in services sectors whereas firms that trade tend to be larger, more established and tend to export goods rather than services.

In Latin America, women-led businesses surveyed on Facebook are smaller than those led by men (Figure 3.3). In particular, microenterprises (defined as firms with fewer than ten employees) represent 68% of the total of women-led firms, whereas this is only 56% for men-led ones. Similarly, large businesses (defined as firms with more than 250 employees) account for 8% of the total of women-led firms, compared to 17% for their men-led counterparts. Even in services sub-sectors where women entrepreneurs represent a majority, such as health, education and personal services, their businesses are generally smaller than those led by men.

Note: This graph shows, for businesses with an online presence on Facebook, what share indicated their firm engages in exports, as opposed to only selling domestically.

Note: This graph shows the distribution of firms across different size categories for businesses with an online presence on Facebook, averaged across the seven Latin American countries covered in this review. Micro firms are those with fewer than 10 employees, small businesses have between 10 and 49 employees, those with 50 to 249 employees are in the medium category, and lastly firms with over 250 employees are considered large.

Gender differences associated with the size of businesses led by men and women entrepreneurs can partly explain the observed export gender gap since smaller enterprises tend to trade less. This is in part because SMEs have fewer resources to meet the high initial costs often associated with engaging in international markets. Smaller firms also face greater challenges than larger firms in navigating foreign markets, with less capacity to address complex regulatory requirements.

Country level differences in the firm size distribution can also partially explain differences in the export gender gap. In Mexico, for instance, women-led businesses are more strongly concentrated in microenterprises, which may contribute to the larger gender export gap in that countries. On the other hand, Colombia shows more balance in the size of firms between men and women entrepreneurs and a lower export gender gap.

Of the firms with a presence on Facebook, women predominantly lead businesses in services sectors, with over 90% of the surveyed women-led firms in services compared to 76% of men-led firms. Specifically, the services subsectors where the greatest share of businesses are led by women are health, education and personal services. Conversely, men led firms represent a clear majority in the utility, agriculture and manufacturing sectors as well as in professional services (Figure 3.4).

The way in which men and women-led businesses are distributed across economic sectors plays a crucial role in explaining the export gender gap in Latin America. Firms in service sectors are less involved in international trade compared to firms that produce goods. Policy barriers to services trade1 are typically higher than barriers to trade in goods, so fewer services firms are generally engaged in exporting than firms in other sectors (Egger et al., 2021[3]) (Benz and Jaax, 2020[4]). The concentration of women-led businesses in services therefore contributes to their lower levels of trade compared to men-led firms.

Note: This graph shows the share of businesses with an online presence on Facebook that indicate having mostly women in their leadership, mostly men, or about equal numbers of men and women.

Notably, there are some heterogeneities at the country level, with women leading a higher proportion of firms in highly traded sectors such as manufacturing in some countries. This can partly explain the lower export gender gap in Brazil and Peru where women-led businesses represent 55% and 23% respectively of the firms operating in the manufacturing sector. This data confirms findings for Peru that suggest that women-led firms are most present in textiles and clothing sectors, followed by food and beverages (Bircher et al., 2020[5]). In Brazil, although women are more represented than in the other Latin American countries under review, they remain largely underrepresented in goods exporting firms. Although not strictly comparable, a study using comprehensive administrative data for goods exporting firms in Brazil found that only 14% of those firms were led by women, and the share of women leaders was inversely proportional to the size of the firm (Ministério da Indústria Comércio Exterior e Serviços, 2023[6]).

Women-led firms surveyed on Facebook are also younger than those led by men, whereas exporting is done more by firms that are larger and more established. Additionally, women enterprises are 10 percentage points more likely to export only to individual consumers instead of to other businesses than men leaders (56% vs 46%). However, some other characteristics of women and men entrepreneurs do not seem to explain export gender gaps. Regarding educational attainment, for example, 50% of women entrepreneurs have completed a university or college degree compared to 46% of men, suggesting that lack of formal training is not what is holding women back from exporting.

Unpacking the importance of firms’ characteristics on the gender export gap in Latin America using a Kitagawa-Oaxaca-Blinder decomposition2, 40% can be attributed to the smaller average size of women-led firms, 22% is due to the concentration of women-led firms in industries less inclined towards international trade such as services, and 6% of the variation has captured the country of activity. This leaves a remaining 32% that cannot be explained by firms’ features.3 Another aspect of firm characteristics that was tested was the age of the firm but its impact on firms’ export performance was found to be negligible. Although difficult to measure, the share of the gender export gap not captured by firm characteristics could conceivably be attributed to factors such as unconscious bias, or a reticence on the part of women business leaders to take the risks that entering international markets entail due to information gaps that they cannot fill through wide professional networks. It was not possible to test such hypotheses due to lack of data.

Women entrepreneurs may face different types of challenges when it comes to growing their businesses and expanding into foreign markets. When asked about the general challenges encountered by businesses, both men and women leaders reported facing difficulties in innovating and securing financing as primary challenges. Given that productivity significantly influences exporting, inadequate financing and sub-optimal innovation can hinder efforts to engage in trade activities.

Access to finance is a well-known challenge for women-led firms. Overall, women-led firms in the seven Latin American countries with an online presence on Facebook are 8 percentage points less likely to receive external funding compared to their male-led counterparts. In Argentina, Chile and Peru, the proportion of women-led firms benefiting from bank loans is 9 to 10 percentage points lower than that of men-led firms. In Chile, women-led firms are roughly 10 percentage points more likely to report encountering challenges with business financing than their men-led counterparts. In Colombia, during a round table of women entrepreneurs, two-thirds indicated that they were self-financed, and did not use bank loans, credit programmes, or any other type of external financing. Women in rural areas may be even less able to access financial services for exporting. During round tables with women entrepreneurs in Peru, business leaders indicated difficulty in financing exports through banks in the Amazon region, or even obtaining letters of credit. Moreover, in some countries interest rates on small loans are prohibitively high with instances of rates over 20% per year. These findings suggest that the gender export gap could be reduced if financing was more accessible for women business leaders.

In some industries such as agriculture, manufacturing, wholesale and retail, women business leaders are more likely to report issues related to securing financing for everyday activities compared to their male-led counterparts. Securing adequate funding is also a problem experienced by male entrepreneurs, but primarily for expanding their business rather than daily operations. Considering that the sectors in which gender differences regarding financing is most pronounced are also those with the highest propensity to trade, closing those gaps could likely reduce the gender export gap.

These results confirm other studies that show for example that only 12% of women-led firms currently have a bank loan compared to 20% of men-led firms (International Trade Centre, 2015[7]). This complements other findings such as in the European Union, where women entrepreneurs are 25% less likely than their male counterparts to use bank loans to fund their business. Even when they receive external finance, women entrepreneurs typically receive smaller amounts, pay higher interest rates, and are required to secure more collateral (OECD, 2022[8]). Moreover, women-owned firms generally face 50% more rejections in their applications for accessing trade finance than men-owned businesses (Korinek, Mourougane and van Lieshout, 2023[9]).

A study carried out by the FAIR Center for Financial Access, Inclusion, and Research in the Tecnológico de Monterrey and Pro Mujer organisation, 73% of women entrepreneurs in Latin America are unable to access financial institutions due to gender-related stereotypes, lack of affordable financial tools, lack of financial literacy and financing procedures that are not tailored to their needs.4 A survey of women-led firms undertaken in Pacific Alliance countries (Chile, Colombia, Mexico and Peru) from 2016 to 2020 found that 57% of firms were self-financed, and only 18% had obtained credit from a financial institution (Bircher et al., 2020[5]).

When specifically asked about challenges they face in international trade, men- and women-led businesses on Facebook generally identified similar obstacles (Figure 3.5). However, women entrepreneurs more often cite issues such as a lack of understanding of foreign markets and difficulties in finding business partners abroad. These challenges are possible reflections of a broader informational gender gap. One way of addressing this issue is through engagement in professional networks, which foster the exchange and dissemination of information. However, when entrepreneurs were questioned about the professional networks they participate in, the absence of good networks available to women-led firms stood out. Furthermore, women are more likely to be part of professional networks with firms that are less relevant for international trade, such as leaders of small-size firms or other women leaders. This may suggest a role for strengthening such networks in closing the export gender gap.

Regulatory uncertainty in foreign markets was a challenge also expressed by women business leaders in all the round tables organised in the region. This challenge was felt especially strongly in some industries such as food and agriculture, technology and the medical sector where trade regulations may be particularly prevalent. Some women business leaders had received advice and assistance from export promotion agencies to navigate regulations in foreign markets, particularly in Colombia and Costa Rica. The entrepreneurs also indicated that they were at a disadvantage when compared to similar firms in larger countries such as Brazil where firms can take advantage of economies of scale in their internal market that is better known to them, even before entering on international markets. Some participants suggested that in some industries Brazilian competitors had substantial technical support by the Brazilian export promotion agency. Lack of information about foreign markets was also one reason given by many business leaders who did not export as to why that was the case.

Note: This graph shows the share of businesses with an online presence on Facebook in the seven Latin American countries covered by this review that indicate having encountered a particular challenge when selling to clients abroad. Only businesses engaged in exporting were asked this question, and respondents were allowed to select multiple options.

Women business leaders expressed the availability and cost of logistics and transportation services as being a keen challenge to exporting and selling their products in more distant markets. The cost of transport and logistics was substantial in Colombia and Costa Rica, for example, and in Costa Rica some small business owners aimed to team up with others exporting to the same destination. Such solutions may be more challenging to rely on in the longer term, however, and a market-based solution could further lower barriers to entry on international markets by small firms (Chapter 5).

One aspect came out particularly strongly in Mexico. Mexican entrepreneurs identified one of their main concerns in exporting, or even getting their goods to marketplaces within Mexico, as security. This issue also plagues large firms distributing their products in Mexico such as supermarket chains and soft drinks, who apparently move about the country in caravans with security personnel. Substantial costs for security personnel, surveillance mechanisms and insurance are more difficult to absorb by small firms. They may be less able to navigate extreme uncertainty and higher risk levels brought on by insecurity. Such issues may also be expressed more keenly by women business leaders who may feel more vulnerable in instances of potential use of force or violence.

Evidence shows that firms with an online presence are more likely to engage in international trade compared to those without (Suominen, 2018[10]). Moreover, digital tools like webpages are linked to a higher propensity to export among women-owned SMEs compared to those owned by men, and digitally enabled trade has been growing faster than non-digital trade (OECD, 2023[11]). Similarly, in Latin America, participation in the ConnectAmericas online platform is associated with a significantly larger increase in exports for women entrepreneurs than for men-led firms in otherwise identical products and destinations (Poole and Volpe, 2023[12]).

Women-led firms responding to the Facebook survey show a higher propensity for utilizing digital platforms in their business activities. Women entrepreneurs also exhibit a more intensive use of digital tools. For instance, approximately one-third of women entrepreneurs in LAC report that more than 75% of their sales orders are made via online platforms, compared to only one-fifth for male leaders. However, women-led businesses more frequently report that a lack of good internet access as an obstacle to their participation in international trade compared to their men-led counterparts, this issue being particularly pronounced in Argentina, Chile, and Colombia. Therefore, the competitive advantage that women leaders may obtain due to their strong embrace of digital technologies seems to be limited in part by inadequate infrastructure.

The seven Latin American countries reviewed generally have a high level of internet coverage overall (Table 3.1). However, internet access in rural areas is low in some countries suggesting that firms outside urban centres may be constrained in their business activities by slower or less reliable access. Given that women-led firms are generally less well financed than their male counterparts, the cost of broadband access can be particularly significant for them. In all seven countries, the cost of fixed broadband access as a percentage of gross national income per capita is substantially higher than in the United States, for example, and in some countries it is multiple times higher. This will impede access to faster networks for smaller, more cash-strapped firms such as some of those owned and led by women.

Many more women expressed that internet access was a major challenge to trade in the two countries that have the highest cost of fixed broadband expressed as a share of per capita national income. In Colombia, 14% of women business leaders and 2% of men leaders indicated that internet access impeded their ability to trade. In Argentina, 12% of women business leaders and 3% of men leaders indicated that internet access impeded their ability to trade. In all other countries covered, gender gaps are smaller and internet access is generally less of an issue. Argentina and Colombia are the two countries in the Review that have the highest fixed broadband cost relative to national income (Table 3.1). In Peru, lack of access to digital networks came out as an issue in a round table with women entrepreneurs that live outside the capital city.

Source: International Telecommunications Union (ITU) Digital Development Dashboard, https://www.itu.int/en/ITU-D/Statistics/Dashboards/Pages/Digital-Development.aspx, accessed 4 April 2024.

Notably, none of the participants to the round table of women entrepreneurs in Colombia indicated that they did not want to expand their business abroad, that they did not want to take the risk involved with exporting, or that they did not want to take time to travel. Only one participant indicated that she did not have sufficient language skills to engage in trade. A survey among the Pacific Alliance countries also found that women business leaders that did not already export expressed a strong interest in doing so (Bircher et al., 2020[5]).Therefore, the desire to export and to assume the risks and time commitment that this entails is prevalent among these women business leaders.

Women often report that they do not have the skills required to pursue entrepreneurship despite that they have higher levels of education on average. Women tend to have less experience in self-employment and continue to have fewer opportunities than men in management positions, which acts as a barrier to gaining management experience and skills that are useful for entrepreneurship (OECD, 2019[13]). Since management skills are often similar to skills needed to successfully manage a business, women’s relative lack of experience in leadership positions can impact the success of their businesses and their ability to engage on international markets.

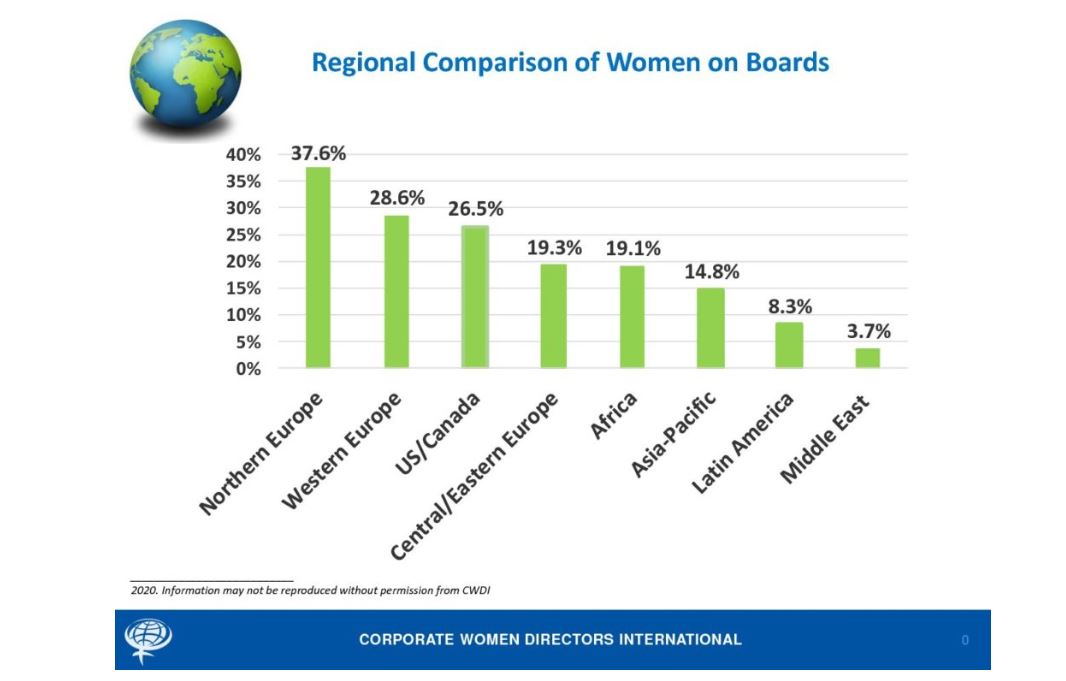

The organisation Corporate Women Directors International estimated in 2020 that only 8.3% of corporate board positions were held by women in Latin America. This was the second lowest region in the world, with only the Middle East having fewer women on boards. This compared with 38% of female board members in Northern Europe, 29% in western Europe, 27% in the United States and Canada, 19% in Africa and 15% in Asia-Pacific.5

Women’s participation on boards in Latin America is far below levels in North America. Women represent between 12% in Mexico and 21% in Colombia; that compares with women’s participation on boards of 35% in Canada and 32% in the United States, and 30% in the OECD on average (Figure 3.6). Despite these low levels comparatively, there has been a recent sharp increase in the number of women on boards in a few Latin American countries: in Chile the share of women in the largest publicly listed companies rose from 10% in 2020 to 17% in 2022; in Colombia from 13% (2020) to 21% (2022); and in Brazil from 14% (2020) to 19% (2022).6 Some countries such as Colombia, Mexico and Peru have instituted targets for women’s participation on boards, where the objective is to reach 30% by 2030 (Frohman and Olmos, 2023[14]). However, many firms still have no women on their boards: in one survey, 27% of firms in Mexico, 17% of firms in Chile and 9% of firms in Brazil have no women on their boards (MSCI, 2022[15]). By contrast, in the United States, out of 593 firms surveyed, only one had an all-male board.

Some evidence suggests that women in senior management positions in large firms in Latin America are even more rare. A survey of 710 firms in Latin America by the Colombian diversity specialist Aequales suggests that fewer women are represented at the highest level of management (CEO or equivalent) compared with board participation. Among Aequales survey respondents, in 22% of firms a woman is at the highest level of management compared with 31% of women in board positions (Aequales, 2022[16]).7

A survey of 120 Mexican firms by McKinsey found that 10% had a woman CEO, and 10% of other C-suite positions were filled by women (McKinsey and Company, 2022[17]). Moreover, the vast majority of women leaders of large firms in Mexico are employed in multi-national firms. About one-third of subsidiaries of foreign firms are headed by women compared with very few (close to 1%) women leaders of Mexican firms.8 Many subsidiaries of foreign firms and multinational firms have (unpublicised) targets for women in leadership and management positions. In some firms, these targets are monitored, reviewed and augmented every year. Some leading firms in terms of gender equality monitor diversity by level and department and link gender targets to managers’ evaluation; some require at least one female candidate in external recruitment processes (McKinsey and Company, 2022[17]). Conversely, many large Mexican firms are either family-owned or family-controlled and leadership is often passed from father to son or nephew.

The greater visibility and demand for more women in high decision-making positions has generated networks that support and train women in senior leadership. Networks such as REDMAD in Chile and ANDI in Colombia offer training to senior women managers on technical issues, management and leadership. However, training and networking are only some aspects that support advancement of women. Others include sponsorship, mandatory disclosure of gender balance on boards and in senior management, and targets or quotas for board diversity.

Notes: Women’s participation on Boards of Directors refers to all members of the highest decision-making body in the given company, such as the board of directors for a company in a unitary system, or the supervisory board in the case of a company in a two-tier system.

Sources: MSCI Women on Boards: Progress Report 2022, except Argentina; data on women on boards are based on gender reports on Boards of Directors in publicly listed companies carried out in by the CNV, which calculated women’s participation on Boards of Directors in all listed companies and Costa Rica, data on women’s participation on Boards of Directors in publicly listed companies was provided by SUGEVAL.

OECD Corporate Governance Factbook (2023), https://www.oecd.org/corporate/corporate-governance-factbook/. Data is for 2022.

In Latin America, informality plays a relevant role in the overall economy.9 Trade and informality can influence one another in a multitude of ways. Often, formal registration is necessary to start trading in order to engage with customs agencies or to receive payments at a distance. Thus, informality is a barrier for firms to start engaging with foreign markets. The reverse relationship may also exist; a rise in productivity as a result of increased trade may be associated with a diversification of the economy moving towards higher productivity sectors, which leads to a higher share of formal firms and to stronger and more sustained growth and development. However, the effect of trade openness on informality varies across countries and other factors such as local institutions may play an even bigger role.10 High levels of informality create disincentives for firms to formalise if they must compete with informal firms that do not pay income and payroll taxes. High levels of informality also impact the potential for firms to prove sustainability throughout their supply chains, which they are increasingly required to do. Firms that use inputs from the informal economy are increasingly challenged to respond to such demands.

In order to shed some light on the potential characteristics of informal firms in LAC, and their attitude towards export, questions from Facebook survey can be used to construct a proxy indicator for informal businesses. The informality proxy is based on four key questions: whether the business receives outside financing; government support during the past months; firms that employ more than five individuals; and firms that have operated for over five years. Firms answering “No” to all these questions are considered as most likely to be informal, while those answering “Yes” at least one time are more likely to be formal.

It is well-documented in the literature that the extensive margin of informality declines with firm size, that is, the share of informal firms declines as firms grow larger (Ulyssea, 2020[18]). One reason for this is that the probability of detection increases with size as larger firms are more visible to the government. More broadly, the opportunity costs of operating in the informal economy are likely to increase with firm size as larger firms might have greater need of accessing formal credit markets. Although there is less evidence on the age of firms, one study using data from Brazil suggests that both the extensive and intensive margins of informality decline with firms’ age, i.e. the number of firms employing informal workers is reduced, and the share of informal workers within firms also decreases (Ulyssea, 2020[18]).

Across the seven Latin American countries under analysis, approximately 13% of surveyed firms with a Facebook presence were identified as most probably informal.11 On average, women-led firms are 9 percentage points more likely to have indicators of informality compared to their men-led counterparts: over the total of women-led businesses surveyed, 18% are proxied as informal, with this percentage decreasing to 9% for their men-led counterparts. Firms proxied as informal operate in their majority within service sectors as wholesale and retail, other services and personal services, whereas a smaller percentage of them is present in sectors such as agriculture and health and education services.

When asked about the general challenges they face, informal firms are more likely to cite difficulties in obtaining adequate financing, both for daily operations and expansion purposes. This challenge is particularly pronounced for informal businesses led by women compared to those led by men. As expected, informal firms are also more likely to report issues in understanding government regulations and tax rules compared to formal ones. The lack of clarity in regulations may partly explain why these firms operate within the informal economy and could present additional obstacles in their transition towards formality.

Firms that trade are substantially less likely to operate within the informal economy.12 Among other reasons, exporting requires strict adherence to official requirements which may incentivise businesses towards formality. Firms that are proxied as more likely to be formal are approximately 12 percentage points more likely to engage in trade compared to their counterparts operating in the informal economy. Specifically, only 3% of enterprises proxied as informal export while this number rises to 15% for formal businesses. Moreover, gender disparities persist in this context: men led businesses, whether formal or informal, show a higher inclination towards exporting than those led by women (Figure 3.7).

Note: This graph shows the share of businesses with an online presence on Facebook that indicate that they engage in export, broken down by firms that are likely to be formal and firms that are likely to be informal according to the proxy developed by the authors.

Tackling informality is complex and requires engaging a comprehensive set of policy levers.13 This analysis suggests that the potential gains from trade could be an incentive for firms to formalise. Programmes to encourage formalisation could be combined with efforts to promote exports and bring firms to export readiness.

References

[16] Aequales (2022), Ranking PAR 2022: The Gender Equity and Diversity Iceberg in Latin America, Aequales, https://empodera.org/impact/en/experiences/experience/aequales-ofrece-herramientas-para-garantizar-un-mundo-laboral-libre-a-traves-de-la-equidad-de-genero-y-diversidad-en-latinoamerica.

[4] Benz, S. and A. Jaax (2020), The costs of regulatory barriers to trade in services: New estimates of ad valorem tariff equivalents, https://doi.org/10.1787/bae97f98-en.

[1] Bernard, A. (2007), “Firms in International Trade”, Journal of Economic Perspectives, Vol. 21/3, pp. 105–130, https://doi.org/10.1257/jep.21.3.105.

[5] Bircher, M. et al. (2020), Estudio de Diagnóstico Radiografía de la participación de las mujeres empresarias de la Alianza del Pacífico en el comercio exterior, Inter-American Development Bank and ConnectAmericas, https://alianzapacifico.net/wp-content/uploads/Estudio-de-Diagnostico-Participacion-de-las-mujeres-empresarias-de-la-AP-en-el-comercio-exterior-NOV2020.pdf.

[3] Egger, P. et al. (2021), “Trade costs in the global economy: Measurement, aggregation and decomposition”, WTO Staff Working Paper, https://doi.org/10.30875/e6c4c0b1-en.

[14] Frohman, A. and X. Olmos (2023), Diagnóstico y estrategía para la participación de las mujeres en cargos de liderazgo y toma de decisiones en las negociaciones internacionales y comerciales de la Alianza des Pacifico, https://alianzapacifico.net/en/diagnosis-and-strategy-for-the-participation-of-women-in-leadership-and-decision-making-positions-in-the-pacific-alliance-presented/.

[20] ILO (ed.) (2023), Has trade led to better jobs?, https://www.ilo.org/resource/integrating-trade-and-decent-work-1.

[7] International Trade Centre (2015), Unlocking Markets for Women to Trade, https://intracen.org/resources/publications/unlocking-markets-for-women-to-trade.

[9] Korinek, J., A. Mourougane and E. van Lieshout (2023), Women are less engaged in trade: Why and what to do about it, VOX CEPR, https://cepr.org/voxeu/columns/women-are-less-engaged-trade-why-and-what-do-about-it.

[17] McKinsey and Company (2022), Women Matter Mexico 2022: Uneven Parity, McKinsey and Company, https://www.mckinsey.com/featured-insights/diversity-and-inclusion/women-matter-mexico-2022-uneven-parity.

[6] Ministério da Indústria Comércio Exterior e Serviços (2023), Mulheres no Comércio Exterior: Uma Análise para o Brasil, https://www.gov.br/mdic/pt-br/assuntos/comercio-exterior/estatisticas/outras-estatisticas-de-comercio-exterior-1/mulheres_comercio_exterior_uma_analise_para_o_brasil.pdf.

[15] MSCI (2022), Women on Boards: 2022 Progress Report, https://www.msci.com/research-and-insights/women-on-boards-progress-report-2022.

[21] OECD (2024), Economic Survey of Mexico, OECD Publishing, https://doi.org/10.1787/b8d974db-en.

[11] OECD (2023), Key Issues in Digital Trade, https://www.oecd.org/trade/OECD-key-issues-in-digital-trade.pdf.

[8] OECD (2022), Financing SMEs and Entrepreneurs 2022: An OECD Scoreboard, OECD Publishing, Paris, https://doi.org/10.1787/e9073a0f-en.

[13] OECD (2019), Engaging and Consulting on Trade Agreements, OECD Publications, Paris, https://issuu.com/oecd.publishing/docs/engaging_and_consulting_on_trade_agreements.

[19] OECD et al. (2023), Latin American Economic Outlook 2023: Investing in Sustainable Development, OECD Publishing, Paris, https://doi.org/10.1787/8c93ff6e-en.

[12] Poole, J. and M. Volpe (2023), Can Online Platforms Promote Women-Led Exporting Firms?, Interamerican Development Bank, https://publications.iadb.org/en/can-online-platforms-promote-women-led-exporting-firms.

[2] Schneider, J. (2020), Future of Business Survey Methodology Note, https://scontent-cdg4-2.xx.fbcdn.net/v/t39.8562-6/238554568_111626007787616_5411963469147558965_n.pdf?_nc_cat=103&ccb=1-7&_nc_sid=b8d81d&_nc_ohc=ps-foUjWU30Q7kNvgE4CmXn&_nc_zt=14&_nc_ht=scontent-cdg4-2.xx&_nc_gid=AxONLqRGNayXH8jz6W_uKbq&oh=00_AYD26mm63k8X.

[10] Suominen, K. (2018), Women-led Firms on the Web: Challenges and Solutions.

[18] Ulyssea, G. (2020), “Informality: Causes and Consequences for Development”, Annual Review of Economics 12, pp. 525-546.

← 1. These barriers are covered for the countries under review in detail in Chapter 5: Services trade in Latin America.

← 2. Kitagawa-Oaxaca-Blinder decomposition is a statistical approach developed initially to analyse gender pay gaps and was used to disentangle the extent to which the gap in exporting can be attributed to differences in firm characteristics. When looking at two groups with a different mean on a variable (in this case, share of exporters), this technique disentangles the share of this difference that can be attributed to specific features and the share that remains unexplained.

← 3. Another method for dissecting the components of export probability is through a regression analysis. When correcting for the country, sectors and firm class-size, the leadership gender ceases to be a relevant factor driving export propensity. As highlighted by the reported decomposition, size and sector emerge as main drivers of the export probability.

← 4. Eileen Galván Carvajal et al, 'Emprendedoras en situación de Missing Middle y sus opciones de financiamiento', Pro Mujer, https://promujer.org/mx/es/missing-middle/.

← 5. Corporate Women Directors International, https://globewomen.org/CWDINet/wp-content/uploads/2020/05/Regional-Comparison-2020.jpg.

{kind=link}

← 6. Source: OECD Gender Data Portal, Employment: Female share of seats on boards of the largest publicly listed companies (oecd.org).

← 7. Note that Aequales survey respondents may be more likely to be more diverse as they have self-selected to take the gender and diversity survey. Respondents are mainly from Colombia (252 firms), Peru (197 firms) and Mexico (139 firms).

← 8. These figures are approximate and refer to a point in time (second quarter 2023). They resulted from structured interviews with women leaders.

← 9. OECD et al. (2023[19]). For instance, before the 2019 COVID-19 pandemic, two-thirds of the region’s population depended totally or partially on informal employment, although with considerable variations between countries.

← 10. ILO (2023[20]).

← 11. This is substantially lower than estimates of the actual number of firms in the informal sector which may be between about 25% and 50% in the region. This proxy aims to identify differences in firms that are very likely to be informal compared with those that are less likely to be informal. It should be noted that firms were not asked directly if they were in the informal sector, nor if they paid taxes or were registered. Moreover, since the online survey was administered to firms that have a Facebook business page, they may be slightly more likely to be in the formal sector than the general population of firms since they have engaged on a traceable digital platform.

← 12. World Bank/WTO (2020); IFC (2011).

← 13. A recent report that examines this question is the OECD’s 2024 Economic Survey of Mexico (OECD, 2024[21])